Money in the house

I rounded up all my cash lying around in my JB home. It totalled S$850 and almost RM1,800! I have deposited the Singapore dollars into the bank, leaving just S$100 aside as emergency cash. I am wondering what to do with the Ringgit. It'll take years to spend them.

I also have some small amount of Thai Baht, Renminbi and New Taiwan dollars lying around.

A few years ago, my house was broken into and I lost almost all my spare cash. I do not know how much I lost, but I estimate it to be around S$2,500. It took me over a week to get over it. I was upset because it was an entirely preventable loss. Why did I leave so much cash at home?

After that, I resolved not to leave so much cash around. However, I do not have a Malaysian bank account, that's why the cash started to accumulate again.

Breakdown of CD prices

Price breakdown of a US$15.99 CD. Taken from the 2004 Rollingstone news article "Wal-Mart Wants $10 CDs":

| Costs | Packaging/manufacturing | $0.80 | 10.6% |

| Distribution | $0.90 | ||

| Marketing | Marketing/promotion | $2.40 | 15.0% |

| Dues | Artists' royalties | $1.60 | 16.2% |

| Publishing royalties | $0.82 | ||

| Musicians' unions | $0.17 | ||

| Label's share | Label overhead | $2.91 | 28.8% |

| Label profit | $1.70 | ||

| Retail's share | Retail overhead | $3.89 | 29.3% |

| Retail profit | $0.80 |

You can think of all the what-if scenario yourself.

Accounting for company benefits

Now that I have dealt with vouchers, how about company benefits?

My company allows me to claim approved items. From this year onwards, I will only discount visits to the doctor and dentist, and not the rest (spectacles, lessons and broadband). The reimbursement for the latter will be classified as income.

Another company benefit is (up to) $75 for parking at/near office for drivers without season parking. I classify it as reimbursement.

Accounting for vouchers

I got $50 Taka vouchers for signing up for the Singnet's 3 Mbps broadband plan.

How should I treat the vouchers? Should I discount the broadband plan by $50 and count the vouchers as $50 cash? Or should I leave the price of the broadband plan as-is and treat the vouchers as "free money"?

It is easy to do the latter, as I would have signed up for the broadband plan even without the vouchers. Thus, the vouchers are a bonus and hence "free". The problem with this line of thought is that it is really easy to buy frivolous stuff with free money.

This is not without precedence. The last time I bought my TV, I got $100 NTUC vouchers. This is really the dealer's way of returning $100 to you. At that time, I did not discount the price of the TV.

This time however, I decided to discount the price of the broadband plan and count the vouchers as cash. Hence, the broadband plan will be cheaper by $50 and any frivolous stuff I buy with the vouchers will be recorded as expenses.

Note that I will only discount the price of the item if I am sure I will use the voucher.

Fraudulent credit card transaction

I rarely use my credit card, preferring to pay by NETS. However, I've been using it more frequently to gain points when there is no additional charge. Even so, I've used it only five times.

Imagine my surprise when I logged onto my online account and saw a charge of US$29.99 for a MFI*SOFTWARE DEVELOPER. I don't recall making such a purchase. I immediately called the Customer Service to dispute the charge. As part of the fraud handling process, my card was terminated and a new one sent to me.

It's alright with me to terminate the card, since I don't like the number — it's hard to remember. What if I got a card with a nice number? It would be a pity. I had an older card that I had used for over five years without any problems. However, I only used it for online purchases. I suspect my card number was swiped from one of the retail transactions.

Now more than ever, I have a reason to get two cards, one for online purchases and the other for retail purchases.

Update: it turned out that I did make an online purchase, so it was not a fraudent purchase after all. I made the purchase on behalf of my colleague, that was why I forgot about it promptly!

Is it what you earn or what you save?

An often quoted financial "wisdom" is, "It's not what you earn, but what you save."

Tell that to a person earning $2,000 or less, and he'll disagree. You need a minimum amount for your daily needs. Depending on your lifestyle, you may need $500 to $1,500 for your daily needs in Singapore. Singaporeans have the option of staying with their parents, paying no rent and utilities. Foreigners have these additional expenses. Is it not a wonder that most foreigners become PRs, get married and quickly buy a HDB flat? No one likes to rent as it is money down the drain.

Beyond the first $1,500, it then becomes a lifestyle choice whether to spend or save. That's where "it's what you save" comes in.

Since the median income is $2,220 (Ministry of Manpower, 2007), you'll think it's easy to save $500 to $1,500. However, the bare minimum just allows you a "subsistence" living in Singapore. There are many things one "cannot" do without — like handphone and broadband. And there seems a endless list of gadgets to buy — notebook, camera, TV, speakers and others. And if you have got them all, it's time to upgrade them.

The more you earn, the easier it is for you to save — if you're not the spendthrift type. A perfect example came by last Sunday when a young dentist was featured. He claimed to be frugal and "saved as much as half his income". However, he later mentioned he was paying $5.5k in rent. It shouldn't take you much time to realize he could save at least $5.5k ("half his income"). This is also a good example that as your income increases, your expectations also go up, so you don't always save more. I bet the dentist won't even consider a HDB flat at $1.5k/mth. He will be able to save $4k more!

My expenses from 2003 to 2007

Here are the corrected numbers for my expenses from 2003 to 2007. I first posted this last October, but later I found some mistakes in the dates and categorization.

My expenses have been spiraling upwards. I have made an effort to cut down on frivolous purchases in 2007, but overall expenses still remain high due to vehicle expenses.

| Category | 2003 | 2004 | 2005 | 2006 | 2007 |

|---|---|---|---|---|---|

| Regular | 16,060 | 16,060 | 14,772 | 14,754 | 18,377 |

| Books | 0 | 138 | 0 | 150 | 929 |

| Lessons | 0 | 1,500 | 690 | 1,900 | 380 |

| Anime DVDs | 4,373 | 408 | 1,114 | 383 | 344 |

| Anime (others) | 5,116 | 7,910 | 2,705 | 1,697 | 1,175 |

| DVDs | 509 | 315 | 1,360 | 1,160 | 396 |

| CDs, games, comics | 227 | 638 | 3,120 | 1,335 | 389 |

| Misc | 25 | 29 | 786 | 4,085 | 3,493 |

| Trips | 0 | 0 | 0 | 1,554 | 1,276 |

| Vehicle Purchases | 0 | 3,853 | 1,587 | 7,513 | 31,363 |

| Vehicle Running Costs | 0 | 473 | 1,533 | 2,093 | 9,169 |

Footnotes

- In Singapore dollars. Values are rounded to the nearest dollar.

- Red values are inaccurate. Bolded values are extremely inaccurate.

- Regular expenses are estimated. Public transport, insurance, tax and parents' allowance are included.

- Books do not include art books, model books and magazines. These fall under anime (others) or CD/games/comics.

- Lessons include bike/car lessons.

- Anime (others) contains manga and non-anime toys as well.

- Misc is mainly retail purchases, like electrical appliances, but it includes lavish meals and entertainment too.

- Vehicle purchases include parts.

- Vehicle running costs are road tax, insurance, petrol, parking, servicing and all vehicle related expenses.

Regular expenses are basic expenses. Books and lessons are for self-improvement, hence are positive expenses. The others are all frivolous expenses. Small frivolous expenses are not captured.

"Spend less than what you earn."

I came across a few local blogs that touch on financial topics recently. One thing they mentioned was, "spend less than what you earn". Does anyone not do that? Sure, credit cards allow you to live beyond your means for a while, but how long can you sustain? (For quite a few months, actually, if you get a card each from a different bank, but I doubt you'll last two years of good time — but I'm sure you'll have a decade of agony.)

I suspect what they really mean is, spend much less than what you earn. After all, spending just under your earning doesn't allow you to accumulate your savings.

How difficult is it to save? Let's use the MAS stipulated two-month credit limit as a guide. CPF takes away 20% of your pay, so you're left with 80%. If you're frugal and spend only 30%, you're left with 50%. It will take you four months to save 200% of your monthly pay. If you're the kind of person to bust your credit limit in a week, I doubt you can save 50% of your pay, so just be resigned to a long time of debt.

Replacement time!

There is nothing like having a little bit of spare cash that makes you automatically think of the gadgets you "need" to replace.

Handphone. I have used the same Nokia 6510 handphone for 4-1/2 years. Well, it's small (97 x 43 x 20 mm), light (84 grams) and it still works. That's good enough for me. The only reason why I need to replace it is because the battery doesn't seem to hold charge now and I may not be able to get a replacement battery.

I have ever considered getting a state-of-the-art phone, download the SDK and do some programming myself. Hey, I can even write some useful applications that I can sell! But this remains a dream. (When you program for a living, the last thing you want to do in your free time is to do more programming.)

Notebook. I have used the same Acer Travelmate 611TXV notebook for 6-1/2 years. It has a 850 MHz Pentium III CPU, 512 MB RAM, 40 GB harddisk, 16X DVD/CD-RW drive and 14.1" LCD screen. It runs Windows XP fine, abit on the slow side — I may reinstall it again later this year. The battery doesn't hold charge anymore — it goes flat within 5 minutes. I am thinking of buying a new one. However, the LCD screen has shown signs of weakening. If the LCD screen goes, so does the notebook — as a notebook. I may be able to use it if I get a LCD monitor, but I won't be able to use it as a notebook.

When it comes to notebook, I know exactly what I want: lack of weight. The Acer 611 was 2.26 kg, the lightest 14.1" notebook in its time. My current company's notebook is 1.8 kg, 1.4 kg if you remove the keyboard. My replacement notebook is likely to be a 1.21 kg "traveller". So most likely I'll get an ultra-light notebook. Since the Apple Airbook came out, Sony and Lenovo had also come out with their ultra-light notebooks. I'm considering one of them. I'm also hoping my notebook lasts another year or two so that I can get the second generation of the ultra-lights.

Storage. Storage is a big issue for me. I currently use CD-Rs, but they are awkward for data files larger than 700 MB. I'm considering buying an external DVD-RW drive and/or an external 500 GB hard disk. Hard disks fill up fast if you don't do housekeeping. I already have an external 250 GB hard disk that is 70% filled up.

PC speakers. I am still using my first pair of Labtec PC speakers, bought eleven years ago, in my office. (Over the past years, I have bought three other PC speakers and am still using them on various PCs/notebooks.) This PC speaker is long past its shelf life, but it still gives decent sound at low and normal volumes. What I need is deeper bass and decent sound at high volume — like when I blast the music early in the morning. (By early, I mean 6:30 am.) However, I rarely come to office that early anymore, and my colleagues start to arrive at 7:50 am, so that limits my playing time.

I can do without these new gadgets. I'm happy with my current gadgets. I am using my company's notebook most of the time, so I only need to get a replacement notebook if I leave the company. And even so, my new company should provide me a notebook. As for the storage, I need to put in some effort to clean up the 250 GB hard disk.

Singnet broadband

I just renewed my 3 Mbps broadband contract with Singnet. 512 kbps works equally well for me — I'm a patient surfer and downloader. However, my brother needs 3 Mbps for his streaming videos.

I had no less than seven choices:

- $45/mth: 24-month, ethernet modem, X-box 360 arcade

- $49/mth: 24-month, wireless modem, X-box 360 arcade

- $45/mth: 24-month, ethernet modem, portable DVD player

- $49/mth: 24-month, wireless modem, portable DVD player

- $40.71/mth: 24-month, 50% off first year, ethernet modem

- $44.79/mth: 24-month, 50% off first year, wireless modem

- $43.82/mth: 12-month, one month free or ethernet modem

New subscribers get mio TV. Re-contracters get a $30 or $50 Taka voucher.

Traditionally, I have always opted for the 12-month contract. Broadband prices were supposed to come down significantly every year, but they never did.

I'm usually not interested in bundled gadgets — their specs and accessories often don't match my expectations — so there go four options.

I called up to ask if I didn't want the modem for the 2-year contract (since I already have one), would I get a further discount? Nope. No problem. The current modem takes about 2 minutes to boot up. Let's hope the new one is much faster.

Since I already have a dedicated wireless router, I am not interested in an integrated wireless modem. (I prefer a 2-device setup too.)

Two options left: $40.71/mth 2-year vs $43.82/mth 1-year. Their effective rates were, $30.54/mth and $40.17/mth.

I decided to take up the 2-year contract.

Note that for the Singnet broadband plans, it is necessary to add the fixed line cost ($25/quarter). And don't forget the 7% GST. $30.54/mth becomes $41.60/mth.

This would have been a good time to get the Singtel mobile broadband plan. 512 kbps costs just $11.21/mth, 1.8 Mbps $19.36, 3.6 Mbps $34.65. I can cancel the fixed line too. However, unlike M1, Singtel seems to offer only USB modem. I need an ethernet modem at the least.

What is in my wallet?

From the blog Five Cents Ten Cents (July 2007): "What is inside your wallet says a lot about your attitudes and approach towards financial freedom and what is inside your wallet will always be more important that what you use as your wallet."

If I recall correctly, I paid $22 for my wallet. It took me a while to find exactly the one I wanted — I have very specific requirements for a wallet.

What do I have in my wallet?

- IC

- Driving license

- Malaysia driving license

- 2 ATM cards

- 1 credit card

- 1 cashcard

- S$40

- RM65

- 5 namecards (to give out)

- Office security card

- Kinokuniya membership card

- Vouchers

I do not carry my Malaysia IC with me anymore. Since I usually drive into JB, I keep it in the car. I could do the same for the Malaysia driving license, but since it's just a laminated card, I keep it in the wallet.

I also do not carry around the ez-link card anymore. I almost never take public transport in the past year.

I don't usually carry the Kino membership card with me, it just so happens I have it with me now. I usually put it aside unless I'm sure I'm going to Kino to browse through the books.

I carry two $10 Cold Storage vouchers with me, just in case I want to do some grocery shopping. They are very thin and take up no space at all.

My investment approach

My investment approach is really simple: (i) DIY, (ii) don't lose the capital!, (iii) sound fundamentals and (iv) long-term. I focus mainly on the local equities market. Allow me to quote from Warren Buffet:

- Risk comes from not knowing what you're doing.

- Diversification is a protection against ignorance. It makes very little sense for those who know what they're doing.

- Why not invest your assets in the companies you really like? As Mae West said, "Too much of a good thing can be wonderful".

- Rule No. 1: Never lose money. Rule No. 2: Never forget rule No. 1.

- You only have to do a very few things right in your life so long as you don't do too many things wrong.

- We simply attempt to be fearful when others are greedy and to be greedy only when others are fearful.

- Most people get interested in stocks when everyone else is. The time to get interested is when no one else is. You can't buy what is popular and do well.

- Only buy something that you'd be perfectly happy to hold if the market shut down for 10 years.

- Price is what you pay. Value is what you get.

- In the business world, the rearview mirror is always clearer than the windshield.

Points 2 and 3 are the same. Points 4 and 5 are the same. Points 6 and 7 are the same.

And there you have it. That's my investment approach.

Where is my money?

For the first time ever, I decided to break down my asset for a clearer picture of my net worth.

| Category | 3/2008 |

|---|---|

| Cash | 55.9% |

| Company shares | 7.3% |

| Equities | 8.8% |

| Funds | 6.6% |

| Insurance | 4.2% |

| Material asset | 14.1% |

| Working cash | 3.2% |

Cash is either fixed deposit or just plain bank accounts. This is 100% liquid.

Company shares includes options. I use the current market value. The value is estimated conservatively due to high commissions and volatile exchange rate. Still, it shouldn't be out by 5% (7.3% +/- 0.4%).

For equities and funds, I use the lower of the current market price and the initial purchase price. Unrealized gain is not counted, but unrealized loss is. Commissions are currently not taken into account.

For insurance, I use its current cash value. This figure needs to be updated annually.

For material asset, currently I only count items above $1000 — at their current market value. In the future, I will include the top five items below $1000. I use a conservative estimate of the current market value. Even so, it may take a while — say, two weeks — to sell the items.

Working cash is the cash I put aside for my daily expenses. It can last me a month or two.

I gave out a loan a few years ago. I do not include it because I do not know if it is recoverable.

I do not include CPF as it cannot be used freely.

I do not have any liabilities, so I do not have to worry how to take them into account. I suppose I'll take the outstanding loan minus the cash value or the market value.

With this exercise, now I know where my money is in case I ever need to "run road"! I don't intend to review this very often, perhaps every half a year.

Short term plans

I'll cancel some of my insurance policies and buy purely term ones. I'll do the investment myself, thank you very much.

I'll sell off part of my company options — due to their expiry dates — to lock in their value now.

I plan to reduce the cash to 50% and increase the equities (including company shares) to 20%. I would like to increase it to 25%, but there's nowhere to channel the money from!

Updated (23/4): I have updated the numbers slightly for accuracy.

Updated (5/5): I omitted money from one bank account totally!

Why discount instead of price reduction?

It is usual to see a high price for a handphone or broadband plan and a discount applied to it. No one ever pays the non-discounted price. Why not an outright price reduction then? One obvious explanation is that you only qualify for the discount under a contract. By signing it, you're tied up for a year or two.

How about petrol companies? They offer a standard 5% discount. But they don't offer any contracts. One explanation is that it is easier to vary the discount than the price. Different groups of customers qualify for different discounts, but there's just one petrol price.

Still, you would have thought that the petrol companies want the price to be lower because they have to pay petrol tax to the Government. On the other hand, since they pass the cost to us, they don't really care.

Trading limit

My trading limit is $10k. It was fine cos I didn't buy high priced shares. Recently, I became interested in shares that range from $5 to $10. My low limit means that I'm only able to trade once per three days — the limit is lowered as soon as you bid and goes back up only after you pay up.

Why three days? I can pay by EPS on the same day, except that my main funds are in another bank account and I need to transfer it to the bank account linked to EPS. Maybe I should keep some funds on standby.

My brokage firm declined to increase my limit to $20k, citing volatile market conditions. Damn, I should have increased it last year.

Expenses for Feburary 2008

| Category | Jan | Feb |

|---|---|---|

| Basic | 902.71 | 936.18 |

| Cash | 182.72 | 194.95 |

| Credit Card | 103.10 | 44.00 |

| Vehicle | 282.32 | 830.80 |

| Others | 304.15 | 200.00 |

| Total | 1,775.00 | 2,205.93 |

The basic expenses are higher purely because the phone bills are deducted twice, for this and last month.

Higher cash withdrawal means that I am spending more on food.

I dislike paying by credit card because it screws up my accounting — this month's expenses is reflected in the next month. However, I will use my credit card more often to accumulate points to exchange for shopping vouchers.

I bought some car parts that, hopefully, I will get around to fit them in the next few months.

Two items account for the entire expenditure in Others: a bouquet of flowers at $70, and a bidded bottle of XO at $130.

Vehicle depreciation

YBR125

My estimation of my YBR125's depreciation. I paid $3,853 for it in 12/2004.

| Year | 12/2004 | 12/2005 | 12/2006 | 12/2007 | 12/2008 |

|---|---|---|---|---|---|

| Body | 2,000 | 1,800 | 1,600 | 1,400 | 1,200 |

| PARF | 0 | 0 | 0 | 0 | 0 |

| COE | 701 | 631 | 561 | 491 | 421 |

| Year | 12/2009 | 12/2010 | 12/2011 | 12/2012 | 12/2013 | 12/2014 |

|---|---|---|---|---|---|---|

| Body | 1,000 | 800 | 600 | 500 | 450 | 425 |

| PARF | 0 | 0 | 0 | 0 | 0 | 0 |

| COE | 351 | 280 | 210 | 140 | 70 | 0 |

I estimate a residue body value of $425. This is probably on the high side, but I think it's doable because the bike has pretty low mileage.

The bike will be worth $1,425 after I renew the COE.

CB400F

My estimation of my CB400F's depreciation. I paid $7,400 for it in 4/2006. (Transfer fee absorbed by seller grudgingly.)

| Year | 8/1998 | 8/1999 | 8/2000 | 8/2001 | 8/2002 |

|---|---|---|---|---|---|

| Body | |||||

| PARF | 0 | 0 | 0 | 0 | 0 |

| COE | 700 | 630 | 560 | 490 | 420 |

| Year | 8/2003 | 8/2004 | 8/2005 | 8/2006 | 8/2007 | 8/2008 |

|---|---|---|---|---|---|---|

| Body | 6,000 | 4,000 | 3,000 | |||

| PARF | 0 | 0 | 0 | 0 | 0 | 0 |

| COE | 350 | 280 | 210 | 140 | 70 | 0 |

I estimate a residue body value of $3,000. This is because the bike is pretty rare (in Singapore anyway) and has very low mileage. In comparison, a normal CB400 can ask for $2,000 at the end of 10 years. The bike will be worth $4,000 after I renew the COE.

The bike will be able to command a higher premium if I can find a classic bike enthusiast. Although this bike is not a real classic bike (it is only 10 years old), it is very retro. I have been told many times by strangers at traffic lights, petrol stations and car parks that this bike reminds them of their younger riding days. Nostalgia, that's worth a high premium. (Hey, I paid a premium for this bike too!)

MX-5

My estimation of my MX-5's depreciation. I paid $29,569 for it in 2/2007, including the transfer fee.

| Year | 8/2001 | 8/2002 | 8/2003 | 8/2004 | 8/2005 |

|---|---|---|---|---|---|

| Body | |||||

| PARF | 0 | 0 | 0 | 0 | 0 |

| COE | 18,444 | 16,600 | 14,755 | 12,911 | 11,066 |

| Year | 8/2006 | 8/2007 | 8/2008 | 8/2009 | 8/2010 | 8/2011 |

|---|---|---|---|---|---|---|

| Body | 18,000 | 15,000 | 12,000 | 9,000 | 7,000 | |

| PARF | 0 | 0 | 0 | 0 | 0 | 0 |

| COE | 9,222 | 7,378 | 5,533 | 3,689 | 1,844 | 0 |

I estimate a residue body value of $7,000. The MX-5 commands a premium by virtue of being a convertible. The car will be worth $23,000 after I renew the COE.

It is difficult to estimate the car's residue value due to its niche market. I believe the price will be $25k to $30k in early 2008, then drop to $20k to $25k in late 2008 and 2009. It'll then drop to $15k to $20k in 2010 and finally to $10k to $15k in 2011. This is because, when combined with COE, the car ends up at the $25k to $30k mark, which may be the sweet spot for low-end convertibles — the demand keeps the price there, any lower and there will be too many buyers.

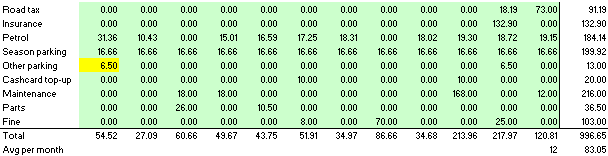

Vehicle expenses for 2007

YBR125

The YBR125 would have been cheaper if it weren't for servicing and the fines. The servicing was unavoidable — some parts had reached end-of-life after 3 years. The fines were entirely avoidable.

I don't foresee any major spending this year.

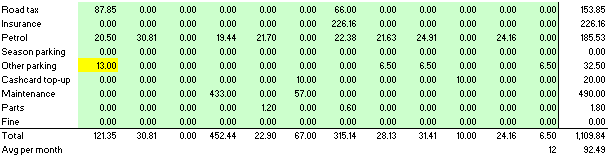

CB400F

The servicing was necessary due to wear-and-tear of old parts. I don't expect any parts to fail this year.

It is necessary to renew the COE this year.

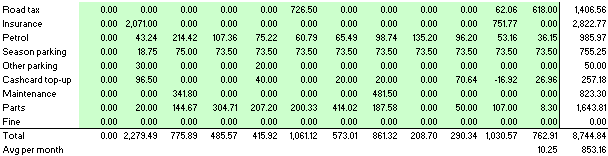

MX-5

I owned the MX-5 for only 10.25 months last year, so the average expenses per month was calculated as such. I had to pay the insurance a second time to align it with the road tax.

The servicing and maintenance will remain high this year. The work never ends on the MX-5 — there are just too many things to change! There are already a few known expenses; the highest is expected to be the tyres.

Notes:

Yellow means estimated.

Road tax includes inspection as well.

Other parking is HDB/URA parking coupons.

Cashcard top-up tracks cashcard usage. It can be negative because I get reimbursed up to $75 for parking at my office.

Maintenance is sending the vehicle for servicing/repair.

Parts are stuff that I bought and changed myself.

Expenses for January 2008

| Category | Jan |

|---|---|

| Basic | 902.71 |

| Cash | 182.72 |

| Credit Card | 103.10 |

| Vehicle | 282.32 |

| Others | 304.15 |

| Total | 1,775.00 |

A pre-ordered toy arrived and, at $260, it accounted for the bulk of Others.

Update: I realized I did not take reimbursement into account properly. The figures have been corrected.

How long can you hold out?

Suppose you stopped working, how long can you hold out? Now that the recession is upon us, it's important to make sure your savings can last 3 to 6 months.

How Singapore is run

More than ever, recent events confirm my suspicion how the Singapore economy is run. The Government doesn't want you to have a lot of spare cash. Sure, if you are well-off, you can buy quality stuff that improves your quality of life; you just won't have much cash left over. The Government has always tried to make you spend according to your income — HDB has a income ceiling for new flats. High earner but want to save the bulk of it by buying a 3-room flat? Sorry, no can do.

The most recent event is of course the means-testing for health care. "Pay as you can afford it." What is wrong with trying to save money by opting for "subsidized" wards?

The saying "You can't afford to fall sick in Singapore" is now more true than ever. A major illness will bankrupt you before the Government decides you're worth helping. Be sure to insure yourself properly.

Credit Card Points

I used to let my credit card points expire, because I thought it was too troublesome to keep track of them. However, on the last day of last year, faced with 1,630 points expiring, I decided to redeem them.

Looking through the long list of items, I discovered that not all items have the same exchange rate. The usual exchange rate is 2.5 cents per point, but it can range from 2 cents to 3 cents. However, it doesn't mean that a high exchange rate is always better. You got to look at the item's inherent profit margin as well.

I only found two worthwhile items: 400 points for a $10 Cold Storage voucher and 180 points for a $5 Burger King voucher.

After redeeming, I still have 1,518 points left. The very next day, my bank devalued the points. The list of redeemable items also shrunk drastically. There is no more Burger King vouchers and it now takes 575 points to redeem the Cold Storage voucher.

At the end of the day, it's no big deal. It takes $5 to earn one point. That's $2,875 to earn a $10 voucher (used to be $2,000). You lose only a little even if you don't pay any attention to your points.

Expenses for December 2007

My expenses for the past two months. Slightly lower purely because my phone bills were not deducted. This month starts a new cycle for this year.

| Category | Nov | Dec |

|---|---|---|

| Basic | 842.39 | 780.12 |

| Cash | 153.50 | 174.00 |

| Credit Card | 250.09 | 100.39 |

| Vehicle | 1,271.71 | 924.45 |

| Others | 27.96 | 338.74 |

| Total | 2,545.65 | 2,317.70 |

The trial run for these two months has been useful. It highlighted many problems, two of which were beyond my control:

- Wrong transaction dates

- Items that are not billed within the month

I've checked with my bank that the dates are effective transactional dates, so any transfers/transactions done on weekends or public holidays are affected.

Update: I realized I have not take reimbursement into account properly. The figures have been corrected.

(void *) &NHY;